Alright folks, let’s dive straight into the big leagues. Federal Reserve interest rates are like the heartbeat of the U.S. economy, and if you’re paying attention, you’ll realize just how much they shape our financial world. Whether you’re an investor, a homeowner, or even someone who’s just trying to save up for that dream vacation, these rates have a way of sneaking into your wallet one way or another. So buckle up, because we’re about to break down the ins and outs of how it all works.

Now, you might be thinking, “Why should I care about federal reserve interest rates?” Well, the answer is simple: because they affect everything from mortgage payments to credit card interest and even how much money you earn in your savings account. In other words, they’re kind of a big deal. And don’t worry, we’ll make sure to explain it in a way that doesn’t feel like you’re reading a textbook—promise!

Before we get too deep into the rabbit hole, let’s set the stage. The Federal Reserve, often called “the Fed,” is like the financial quarterback of the U.S. economy. Their job? To keep things running smoothly by tweaking interest rates, controlling inflation, and making sure the economy doesn’t go off the rails. It’s a pretty cool gig, if you ask me. But how exactly do they pull it off? Let’s find out.

Read also:Cool Cortes De Pelo Con Rayitos The Ultimate Guide For Stylish Looks

Understanding Federal Reserve Interest Rates: What’s the Big Deal?

Here’s the thing about federal reserve interest rates—they’re not just random numbers floating around in the ether. These rates are carefully calculated by the Fed based on a ton of economic indicators. Think of it like a weather forecast for the economy. If things are looking good, they might lower rates to keep the party going. But if the economy’s starting to overheat, they’ll crank them up to cool things down.

One of the key tools the Fed uses is the federal funds rate, which is essentially the interest rate banks charge each other for short-term loans. This rate has a ripple effect throughout the economy, influencing everything from business loans to consumer credit. So when the Fed decides to raise or lower rates, it’s like dropping a pebble in a pond—the impact spreads far and wide.

How Do Federal Reserve Interest Rates Impact You?

Now, let’s talk about the real-world implications of these rates. For starters, if you’ve got a mortgage, you’ll definitely want to keep an eye on what the Fed’s up to. When rates go up, so does your monthly payment. On the flip side, if rates drop, you might see some relief in your budget. Same goes for car loans, credit cards, and even student loans.

But it’s not all about debt. Savers can also benefit from higher interest rates, as banks tend to offer better returns on savings accounts and certificates of deposit (CDs). So if you’ve been squirreling away cash in a high-yield savings account, a rate hike could mean more green in your pocket. Neat, right?

Who’s Calling the Shots? A Closer Look at the Federal Reserve

Alright, let’s zoom in on the Fed itself. Established back in 1913, the Federal Reserve System is made up of a bunch of different components, including the Board of Governors, the Federal Open Market Committee (FOMC), and 12 regional reserve banks scattered across the country. It’s like a financial ecosystem, each part playing its own role in keeping the economy healthy.

At the helm is the FOMC, which meets eight times a year to discuss monetary policy and set those all-important interest rates. These meetings are basically the Super Bowl of economic news, with analysts and investors hanging on every word to see what the Fed’s next move will be. And trust me, those decisions can send shockwaves through the markets.

Read also:Ghost Face Matching Pfps The Ultimate Guide To Unveiling Digital Identity

Breaking Down the Fed’s Dual Mandate

One of the Fed’s main goals is to maintain stable prices and maximum employment. This is known as their “dual mandate,” and it’s kind of like their North Star when it comes to setting interest rates. If inflation starts creeping up, they’ll tighten the reins by raising rates. But if unemployment’s too high, they might ease up a bit to stimulate job growth.

It’s a delicate balancing act, and the Fed’s got to be careful not to overdo it in either direction. Too much tightening can slow down the economy, while too much loosening can lead to runaway inflation. So they’ve got to play it smart, always keeping an eye on the bigger picture.

Why Federal Reserve Interest Rates Matter for Investors

Investors, listen up. Federal reserve interest rates can have a massive impact on the stock market. When rates are low, borrowing becomes cheaper, which can fuel business expansion and drive up stock prices. But when rates go up, borrowing costs increase, which can put a damper on corporate profits and send stocks tumbling.

Of course, it’s not all doom and gloom. Some sectors, like financials and utilities, tend to thrive in a higher-rate environment. So if you’re a savvy investor, you can use these rate changes to your advantage by adjusting your portfolio accordingly. Just don’t forget to do your homework before making any big moves!

How to Stay Ahead of the Curve

So how can you stay on top of federal reserve interest rates and make informed decisions? First off, keep an eye on the Fed’s statements and press conferences. They’ll often give hints about what’s coming down the pipeline, so you can get a jump on any changes. And don’t be afraid to consult with a financial advisor if you’re feeling overwhelmed—sometimes a second opinion can make all the difference.

Historical Perspective: The Evolution of Federal Reserve Interest Rates

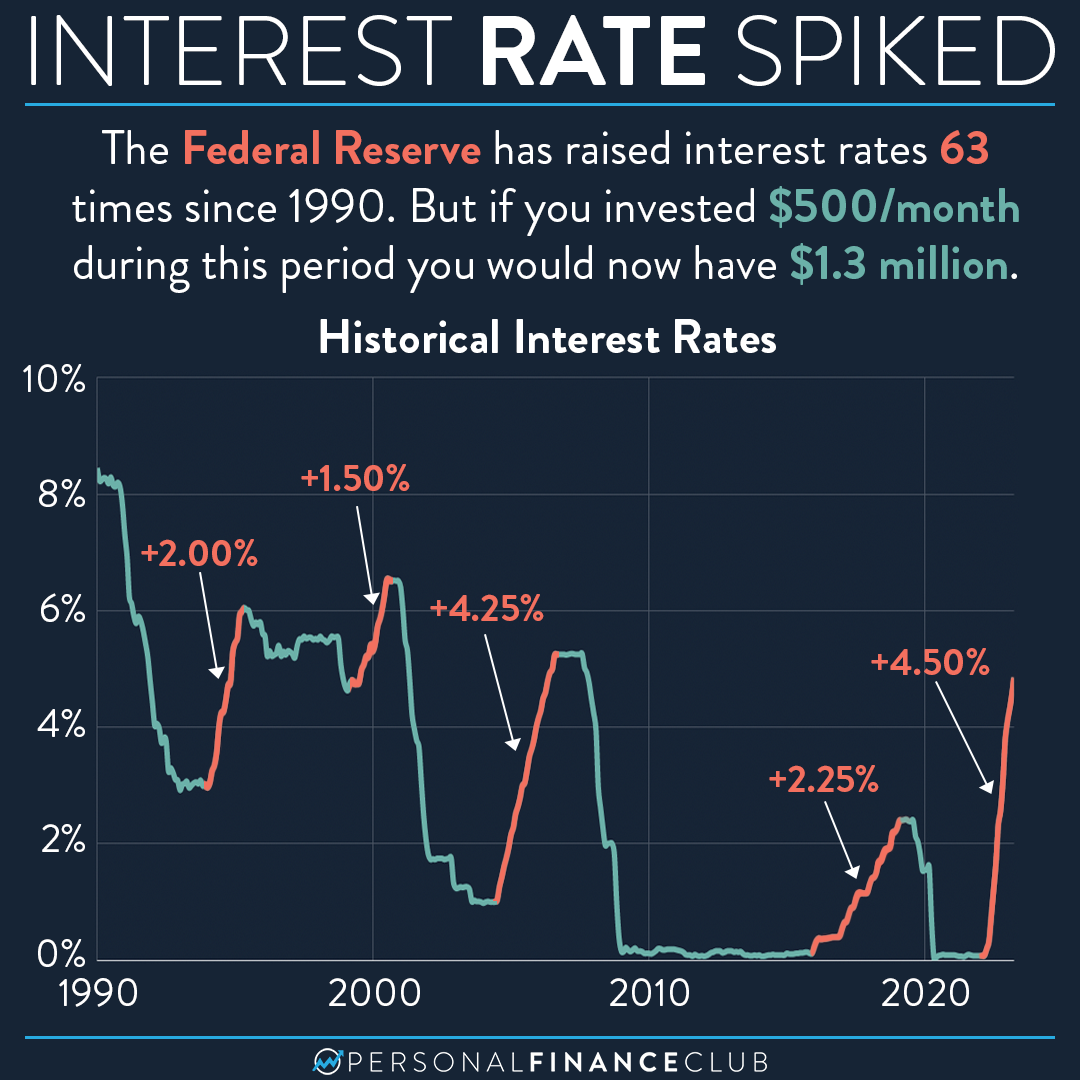

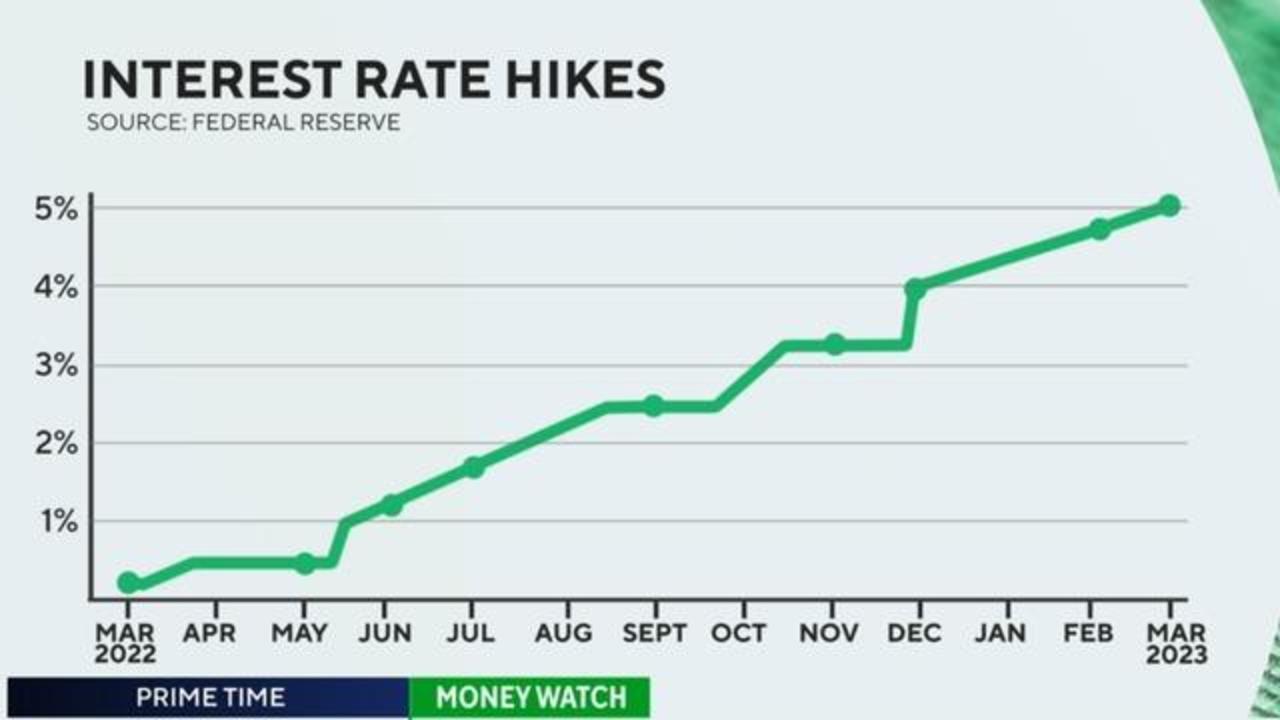

Let’s take a trip down memory lane and see how federal reserve interest rates have evolved over the years. Back in the 1980s, under Chairman Paul Volcker, rates were sky-high as the Fed battled rampant inflation. Fast forward to the 2008 financial crisis, and rates were slashed to near zero in an effort to stabilize the economy. And more recently, we’ve seen rates fluctuate in response to global events like the pandemic and geopolitical tensions.

Each era brings its own unique challenges, and the Fed’s response to these challenges has shaped the economic landscape we see today. By studying this history, we can gain valuable insights into how the Fed operates and what to expect in the future.

Key Milestones in Federal Reserve Interest Rate History

- 1981: The federal funds rate hits an all-time high of 20%, as the Fed fights inflation.

- 2008: Rates are cut to near zero during the financial crisis, sparking a decade of ultra-low borrowing costs.

- 2020: In response to the pandemic, the Fed slashes rates again, injecting liquidity into the economy.

What’s Next for Federal Reserve Interest Rates?

Looking ahead, there’s no shortage of speculation about where federal reserve interest rates are headed. With inflation still a concern and the economy slowly recovering from the pandemic, the Fed’s got its work cut out for it. Some experts predict rates will stay low for the foreseeable future, while others think they’ll need to rise to keep inflation in check.

One thing’s for sure: the Fed’s decisions will continue to shape the economic landscape for years to come. Whether you’re an individual consumer or a major corporation, staying informed about these rates is crucial for making sound financial decisions.

How to Prepare for Future Rate Changes

So what can you do to prepare for potential rate changes? Start by reviewing your current financial situation. If you’ve got adjustable-rate loans, consider refinancing to lock in a fixed rate. And if you’re saving for the future, explore options like high-yield savings accounts or CDs that can offer better returns in a rising-rate environment.

Final Thoughts: Why Federal Reserve Interest Rates Matter

Alright folks, let’s wrap things up. Federal reserve interest rates might not be the sexiest topic in the world, but they’re undeniably important. Whether you’re buying a house, investing in stocks, or just trying to make your money work harder for you, these rates play a critical role in shaping your financial future.

So the next time you hear about the Fed making a move, don’t tune it out. Take a moment to understand what it means for you and your money. And remember, knowledge is power. By staying informed and proactive, you can navigate the ever-changing economic landscape with confidence.

Got any questions or thoughts? Drop them in the comments below, and don’t forget to share this article with your friends and family. Knowledge is contagious, and the more people who understand how the Fed works, the better off we’ll all be. Until next time, stay sharp and keep those wallets fat!

Table of Contents

- Federal Reserve Interest Rates: The Backbone of the U.S. Economy

- Understanding Federal Reserve Interest Rates: What’s the Big Deal?

- How Do Federal Reserve Interest Rates Impact You?

- Who’s Calling the Shots? A Closer Look at the Federal Reserve

- Breaking Down the Fed’s Dual Mandate

- Why Federal Reserve Interest Rates Matter for Investors

- How to Stay Ahead of the Curve

- Historical Perspective: The Evolution of Federal Reserve Interest Rates

- Key Milestones in Federal Reserve Interest Rate History

- What’s Next for Federal Reserve Interest Rates?

- How to Prepare for Future Rate Changes

- Final Thoughts: Why Federal Reserve Interest Rates Matter